Introduction

The best investment options in Kenya have never been more accessible than they are today. Whether you have Ksh 500 sitting idle in your M-Pesa or Ksh 500,000 ready to deploy, Kenya's financial markets now offer a legal, regulated home for your money — one that can grow at rates that no ordinary savings account will ever match.

Think about this: a regular bank savings account in Kenya pays roughly 4–7% per year in interest. Meanwhile, some money market funds are paying over 13%, top NSE stocks are handing out dividends at 8–13% yields, and long-term government bonds are locking in rates above 15%. The gap between "saving" and "investing" in Kenya is enormous — and this guide is your roadmap across it.

In this article, we rank and review Kenya's ten best investment options, explain exactly how each one works, show you realistic returns and minimum amounts, and tell you who each option is best suited for. We are straightforward, evidence-based, and honest about the risks.

Quick Comparison: Top 10 Investment Options in Kenya

| # | Option | Min. Amount | Expected Returns | Risk Level | Liquidity |

|---|---|---|---|---|---|

| 1 | NSE Shares | 1 share | 5–20% p.a. + dividends | Medium | High |

| 2 | Money Market Funds | Ksh 100 | 10–14% p.a. | Low | Very High |

| 3 | Government T-Bills | Ksh 50,000 | 14–16% p.a. | Very Low | Medium |

| 4 | Government T-Bonds | Ksh 50,000 | 13–17% p.a. | Very Low | Low–Medium |

| 5 | SACCOs | Ksh 500/mo | 8–14% dividends | Low | Low |

| 6 | Real Estate | Ksh 1M+ | 6–12% p.a. | Medium | Very Low |

| 7 | Unit Trusts / Equity Funds | Ksh 1,000 | 10–20% p.a. | Medium | High |

| 8 | REITs (NSE-listed) | ~Ksh 20+ | 6–9% p.a. | Medium | High |

| 9 | Chamas (Investment Groups) | Ksh 500+/mo | Varies widely | Medium | Low |

| 10 | Agriculture / Agribusiness | Ksh 10,000+ | 15–40% p.a. | High | Very Low |

The Top 10 Best Investment Options in Kenya

📈 1. NSE Shares (Stock Market)

Buying shares on the Nairobi Securities Exchange (NSE) means owning a piece of a real Kenyan company — like Safaricom, Equity Bank, KCB, EABL, or Co-op Bank. When the company grows, your shares grow in value. When it makes a profit, it may pay you a dividend — real cash sent directly to your bank account, usually once or twice a year.

A landmark rule change in August 2025 dropped the minimum trade size to just 1 unit. That means you can now buy a single Safaricom share for around Ksh 30. The NSE's All-Share Index (NASI) posted a stunning 54.61% year-to-date gain through April 2026, reflecting one of Kenya's strongest bull markets in a decade.

Blue-chip picks like Safaricom (SCOM), Equity Group (EQTY), and Standard Chartered Kenya (SCBK) combine capital growth potential with dividend yields of 3–13%, making the NSE the most versatile wealth-building vehicle in Kenya today. See our guide on the 10 best shares to buy in Kenya for a full breakdown.

✅ Pros

- Dual returns: dividends + price appreciation

- Buy/sell in minutes via M-Pesa

- Minimum of just 1 share

- Fully regulated by the CMA

- Over 60 listed companies to choose from

❌ Cons

- Share prices can fall

- Requires basic financial knowledge

- Brokerage fees apply

- Dividends taxed at 5% WHT (residents) / 10% (non-residents)

KE Offers Verdict

NSE shares are our top pick for Kenyans with a long-term mindset. They combine regulation, liquidity, dividend income, and capital growth in a single instrument — and you can start with pocket change. Best for: patient investors aged 18+, students, salaried workers.

Ready to Buy NSE Shares? Start with Faida Investment Bank

Faida Investment Bank is a CMA-licensed stockbroker trusted by thousands of Kenyan investors. Sign up online in minutes — they open your CDS account automatically, and you can fund it via M-Pesa. No branch visit needed.

→ Open a Free Account with Faida💰 2. Money Market Funds (MMFs)

A Money Market Fund (MMF) pools money from thousands of investors and puts it into safe, short-term instruments — things like government T-Bills, bank deposits, and commercial paper. In return, you earn daily interest that compounds over time. It's like a high-yield savings account, but better.

Top Kenyan MMFs as of 2026 include CIC Money Market Fund, Sanlam Money Market Fund, and Cytonn Money Market Fund — all licensed by the Capital Markets Authority (CMA). Effective annual returns range from 10% to 14%, with interest credited daily to your account. You can withdraw your money in as little as 24–48 hours.

The best part? You can start with just Ksh 100. You can also invest straight from M-Pesa in many funds. For those wondering where to park an emergency fund while it earns, an MMF beats any bank savings account by a wide margin.

✅ Pros

- Start with just Ksh 100

- Daily interest, compounded

- Very low risk

- Easy M-Pesa top-ups

- Perfect emergency fund vehicle

❌ Cons

- Returns lower than equities long-term

- Not protected by KDIC

- Withdrawal can take 1–3 days

🏛️ 3. Treasury Bills (T-Bills)

Treasury Bills are short-term government debt instruments issued weekly by the Central Bank of Kenya (CBK). They come in three tenors: 91 days, 182 days, and 364 days. Because they are backed by the Kenyan government, they carry virtually zero default risk — making them the safest investment in the country.

As of June 2026, T-Bill rates hover around 14–16% per year. You invest at a discount and receive the full face value at maturity. For example, if the CBK auctions a 364-day T-Bill at 15%, you invest Ksh 50,000 and receive approximately Ksh 57,500 at the end of the year. You can apply through the CBK's DhowCSD portal or through your bank.

✅ Pros

- Government-backed — near zero risk

- Attractive rates (14–16%)

- Apply online via DhowCSD

- Interest exempt from WHT for individuals

❌ Cons

- Minimum Ksh 50,000 is high for beginners

- Money locked until maturity

- Rates change weekly at auction

📜 4. Treasury Bonds (T-Bonds)

Treasury Bonds work like T-Bills but have much longer tenors — from 2 years to 25 years. In exchange for tying up your money longer, the government pays you semi-annual interest (called a coupon) at rates typically between 13% and 17% per year. This is effectively a guaranteed income stream for years at a time.

Infrastructure Bonds (IFBs) are a special type of T-Bond with one massive advantage: the coupon interest is 100% tax-free. For higher-income investors, this tax shield can make IFBs the single most lucrative investment in Kenya after tax. They are offered periodically by the CBK and usually sell out fast.

✅ Pros

- Semi-annual coupon payments in cash

- IFB interest is tax-free

- Can be traded on secondary market (NSE)

- Predictable, long-term income

❌ Cons

- Long lock-up periods

- Bond prices fall when rates rise

- Minimum Ksh 50,000

🤝 5. SACCOs (Savings and Credit Co-operatives)

SACCOs are member-owned financial institutions regulated by SASRA (SACCO Societies Regulatory Authority). Over 15 million Kenyans belong to a SACCO. You contribute monthly, earn dividends on your shares (typically 8–14% annually), and can access low-interest loans — often at 1% per month on a reducing balance, compared to banks charging 1.2–1.5%.

Major SACCOs include Mwalimu National (for teachers), Kenya Police SACCO, Stima SACCO (for energy sector workers), and Tower SACCO. There are also open-membership SACCOs that welcome anyone with a valid ID. The discipline of monthly contributions forces savings habits that many people struggle to maintain on their own.

✅ Pros

- Strong dividends (8–14%)

- Access to cheap loans

- Forced savings discipline

- Community support network

❌ Cons

- Shares are illiquid

- Must give notice to withdraw

- Quality varies across SACCOs

🏠 6. Real Estate

Land and property remain a deeply ingrained investment choice for Kenyans, and for good reason. Rental yields in Nairobi's prime suburbs (Westlands, Lavington, Karen) range from 5–8% per year, while satellite towns like Ruaka, Athi River, Kitengela, and Juja have delivered annual capital appreciation of 6–12% over the past five years, according to HassConsult's Kenya Property Index.

The main challenge is the large capital outlay required — most plots or houses start at Ksh 1 million and upward. However, real estate investment trusts (REITs, covered below) now let you invest in property through the NSE from as little as Ksh 20. If you are ready for direct property, buy in fast-growing satellite towns near Nairobi rather than within the city, where land is already expensive but yields are compressing.

✅ Pros

- Tangible, hard asset

- Dual returns: rent + appreciation

- Collateral for bank loans

- Long-term wealth preservation

❌ Cons

- Large capital required

- Very illiquid asset

- Land fraud risks — verify titles

- Stamp duty, legal, agent fees

📊 7. Unit Trusts & Equity Funds

Unit trusts pool your money with other investors and hand management to a professional fund manager. Equity funds invest in NSE-listed shares on your behalf, aiming to beat the market over time. They are perfect for people who want stock market exposure without picking individual shares themselves.

Top fund managers in Kenya include Old Mutual, ICEA Lion, CIC Asset Management, and Sanlam Investments — all licensed by the CMA. Equity funds have historically delivered 10–20% per year over five-year horizons, outperforming most savings products. There is also a growing range of balanced funds (mixing shares and bonds) and income funds for those who prefer steady payouts.

✅ Pros

- Professionally managed

- Low entry point (Ksh 1,000)

- Diversification built in

- Access to offshore funds

❌ Cons

- Annual management fees (1.5–2.5%)

- No guarantee of returns

- Performance varies by fund manager

🏢 8. REITs (Real Estate Investment Trusts)

REITs are listed on the NSE and allow you to invest in large commercial and residential properties without buying a building. You earn a share of rental income and any property value gains. Kenya's main listed REIT is Fahari i-REIT (FAHR), managed by ICEA Lion. REITs must distribute at least 80% of their taxable income to unit holders — making them strong income investments.

Since the August 2025 single-unit rule change, you can buy REIT units on the NSE from just 1 unit, dramatically lowering the entry barrier. If you want real estate exposure but lack the millions for a plot, REITs are your most accessible legal route.

✅ Pros

- Very low entry point via NSE

- Regular income distributions

- Liquid — sell on NSE any day

- No property management headaches

❌ Cons

- Limited REIT options in Kenya

- REIT unit prices can fall

- Yields lower than direct property

👥 9. Chamas (Investment Groups)

A chama is a self-organised group — typically 5–30 members — who pool money regularly and use the funds to invest or lend to each other. Kenya has an estimated 300,000+ registered chamas, collectively managing billions of shillings. Some chamas invest in land, others in the NSE or MMFs, and some run merry-go-round lending cycles.

Well-structured chamas have created genuine wealth — buying land in Nairobi's satellite towns, funding multiple rental properties, and even listing on the NSE as investment clubs. The key is a strong constitution, clear leadership, and professional-grade record-keeping. Chamas that invest in regulated instruments like MMFs, T-Bills, or NSE shares consistently outperform those that rely on informal lending alone. To see what a structured chama can invest in, read our guide on how to buy shares in Kenya.

✅ Pros

- Pool resources for bigger investments

- Social accountability drives savings

- Access to informal credit

- Flexible entry amounts

❌ Cons

- Disputes can destroy the group

- Unregulated if not registered

- Returns depend on members' decisions

🌾 10. Agriculture & Agribusiness

Kenya's agricultural sector contributes over 25% of GDP and employs more than 40% of the workforce. For investors with land or capital, high-value crops like avocados, French beans, macadamia nuts, and tea can deliver returns of 15–40% per year. Poultry farming (broilers and layers) and dairy production also offer strong cash flows when properly managed.

The key to agribusiness profitability is market linkages — selling directly to processors, supermarkets, or export partners rather than brokers who eat most of the margin. Government programmes like AgriBusiness Solutions and contract farming arrangements with companies like Del Monte and BIDCO reduce off-take risk significantly. See our kienyeji chicken farming guide for a practical starting point.

✅ Pros

- Highest potential returns

- Access to government subsidies

- Tangible asset (land/livestock)

- Can scale gradually

❌ Cons

- Weather and pest risks

- Seasonal cash flow

- Requires hands-on management

- Market price volatility

How to Choose the Right Investment for You

There is no one-size-fits-all investment. The right option depends on three things: how much money you have, how long you can leave it invested, and how much risk you can stomach without losing sleep.

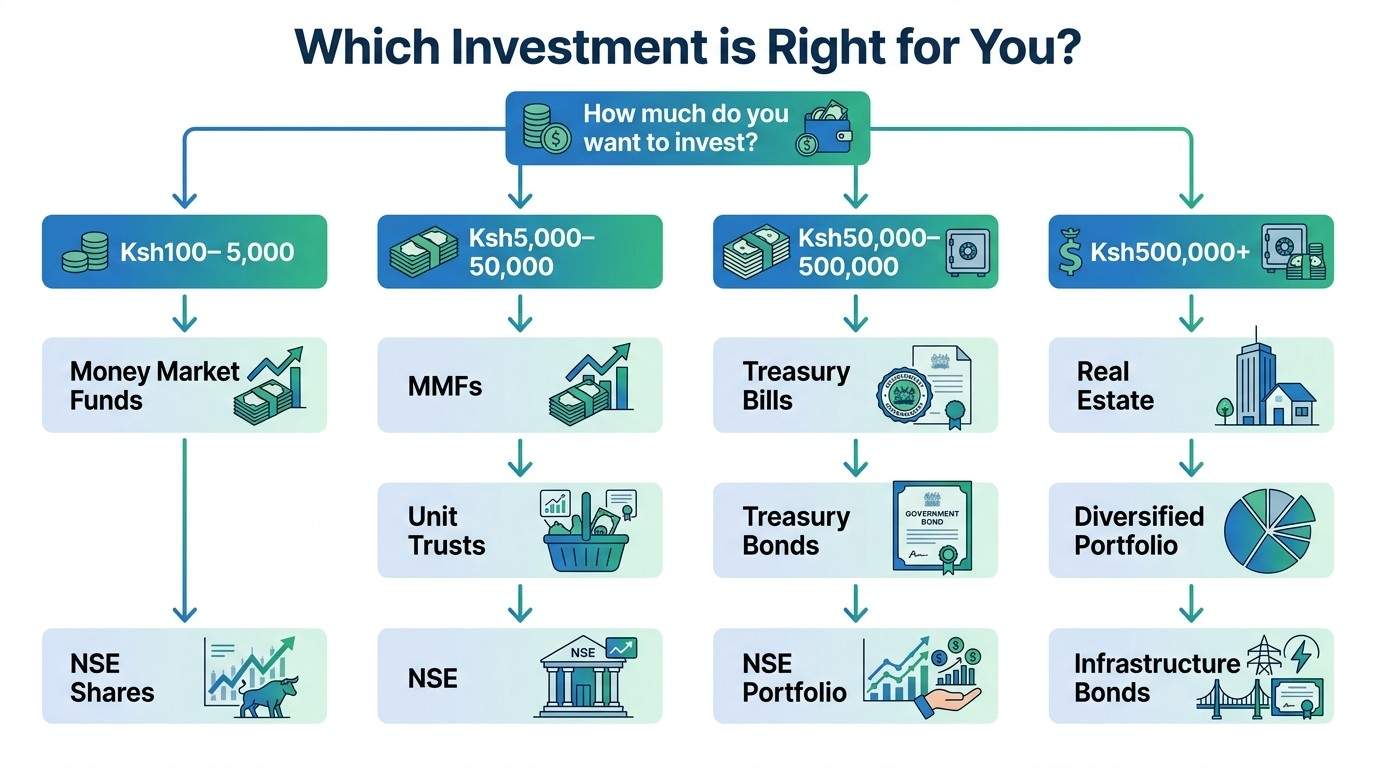

If you have Ksh 100–5,000: Start with a money market fund. It is safe, earns daily interest, and teaches you the habit of putting money to work. Sanlam and CIC are excellent starting points. You can also buy a handful of NSE shares now that the 1-unit minimum rule is in force.

If you have Ksh 5,000–50,000: Consider combining an MMF (for liquidity) with equity unit trusts or NSE shares (for growth). Spreading your money across two vehicles reduces risk while maximising return potential.

If you have Ksh 50,000–500,000: Government securities (T-Bills and T-Bonds) become available to you — and at 14–17% per year, they are extremely compelling. Mix in NSE shares, and you have a balanced portfolio covering both safety and growth.

If you have Ksh 500,000+: Real estate, a diversified NSE portfolio, Infrastructure Bonds, and a SACCO membership can all work together. At this level, consider consulting a CMA-licensed financial advisor to build a proper strategy.

Investing While Running a Side Hustle?

Many Kenyans who invest successfully are doing so with income from multiple streams. Blogging, freelancing, and online work can create extra money specifically earmarked for investing. If you are looking for ways to grow your income base before investing, our guides on how to make money blogging and how to start a blog in Kenya are great practical starting points. Even Ksh 2,000 extra per month, invested consistently in an MMF or SACCO, compounds into significant wealth over a decade.

Deep Dive: Kenya's Best Dividend Stocks on the NSE

If dividend income is your priority, two NSE stocks stand out in 2026. Safaricom paid a record Ksh 2.00 per share in 2026 — a 66.7% jump from previous years — driven by surging M-Pesa revenues and a strong EPS growth of 48% year-on-year. Read our Safaricom dividend payout guide for the full history.

Equity Bank paid Ksh 5.75 per share in 2025 — its highest dividend ever. If you owned 10,000 Equity shares, that was Ksh 57,500 landing in your bank account without selling a single share. Our Equity Bank dividend guide walks you through every payout since 2009 and shows you how to start earning dividends today. To understand which stocks offer the best value on the NSE right now, read our guide on how to spot overvalued vs undervalued stocks in Kenya.

Buy NSE Shares in Minutes — Open a Faida Investment Bank Account

Faida is a CMA and NSE-licensed broker. The signup is 100% online, your CDS account opens automatically, and M-Pesa funding is supported. Whether you want Safaricom, Equity Bank, or KCB shares — Faida gets you there.

→ Get Started with Faida TodayRisks Every Kenyan Investor Must Know

Every investment carries some level of risk. The key is understanding the risks and managing them — not avoiding investing altogether out of fear.

Market Risk: Share prices and REIT values can fall. The NSE saw significant losses in 2022 and 2023 before the 2025–2026 recovery. Long-term investing (5+ years) dramatically reduces the impact of short-term volatility.

Inflation Risk: Money sitting in a low-interest account loses real value every year. Kenya's inflation has historically averaged 5–8% annually. Any investment returning below this threshold is actually shrinking your purchasing power.

Fraud Risk: Always use CMA-licensed fund managers and stockbrokers. Be deeply suspicious of any investment promising returns of 30–50% per month — these are almost certainly pyramid schemes or Ponzi operations. Verify any broker at cma.or.ke.

Liquidity Risk: Real estate, T-Bonds, SACCOs, and chamas can lock your money away for months or years. Always keep at least 3–6 months of expenses in a liquid instrument (MMF or savings account) before committing to long-term investments.

Frequently Asked Questions

What is the best investment option in Kenya for beginners?

How much money do I need to start investing in Kenya?

Are government securities (T-Bills and T-Bonds) safe investments in Kenya?

What is the difference between a SACCO and a bank in Kenya?

How do I buy shares on the NSE in Kenya?

What returns can I expect from real estate in Kenya?

Is it safe to invest in a chama in Kenya?

What is the minimum amount for Treasury Bills in Kenya?

Final Verdict

The best investment in Kenya is the one you actually start. Too many Kenyans spend years researching without ever placing their first Ksh 1,000. The truth is this: even a modest Ksh 5,000 invested monthly in a money market fund at 12% per year grows to over Ksh 2.3 million in 15 years — purely through compounding. Start small, stay consistent, and diversify as your wealth grows.

Our recommendations by stage: beginners → Money Market Fund; intermediate investors → NSE shares + T-Bills; serious investors → NSE + T-Bonds + SACCO + real estate. And for shares specifically, Faida Investment Bank remains our recommended broker for most Kenyan investors.