What Is the Central Bank of Kenya?

Founded in 1966 shortly after Kenya's independence, the Central Bank of Kenya (CBK) was created to replace the East African Currency Board and give Kenya full control over its monetary destiny. Headquartered at the iconic building along Haile Selassie Avenue in Nairobi, the CBK operates under the Central Bank of Kenya Act and reports to the National Assembly, making it legally independent from direct government interference — though in practice the two are deeply intertwined.

Its core mandate is deceptively simple: maintain price stability and foster a sound financial system. But the ripple effects of that mandate touch every household, every matatu ride, every kilo of rice, and every M-Pesa transaction in the country.

Interest Rates & Your Loan Repayments

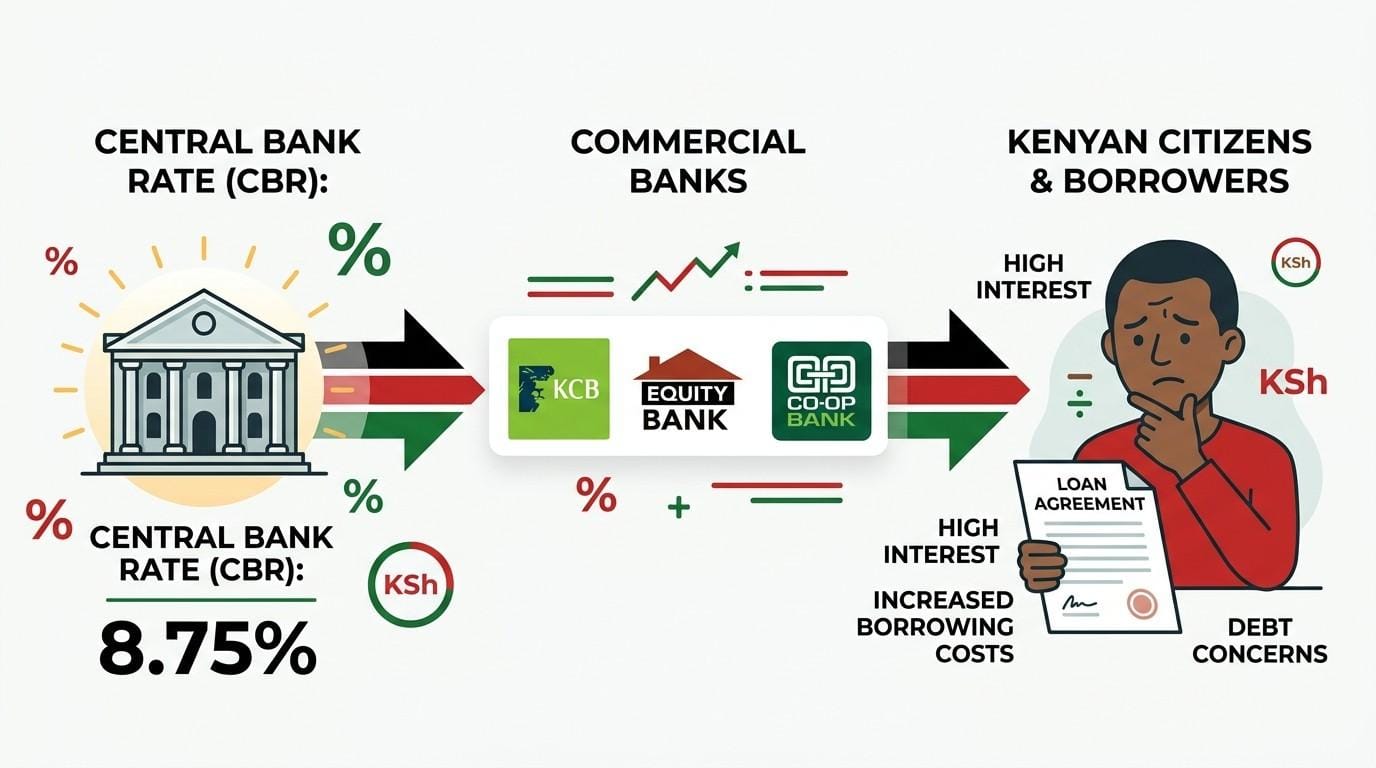

Perhaps the most direct and painful way the CBK reaches into your pocket is through the Central Bank Rate (CBR) — the interest rate at which commercial banks borrow overnight from the CBK. Think of the CBR as the "wholesale price" of money in Kenya. When it moves, everything downstream moves with it.

How the Transmission Mechanism Works

When the CBK's Monetary Policy Committee (MPC) raises the CBR, commercial banks respond by raising their own lending rates. Equity Bank, KCB, Co-op Bank — they all charge you more. Your salary advance costs more. Your car loan becomes pricier. Your mortgage balloons. Conversely, a CBR cut makes credit cheaper, stimulating borrowing and economic activity — though it can also stoke inflation if overdone.

The Interest Rate Cap Saga

Between September 2016 and November 2019, Kenya's Banking (Amendment) Act capped commercial lending rates at 4 percentage points above the CBR. The idea was noble — protect borrowers from predatory rates. But the outcome was perverse: banks retreated from lending to small businesses and individuals deemed "risky," preferring to park funds in Treasury bills and bonds. The cap was eventually repealed, and the CBK returned to using the CBR as its primary rate signal.

"A 100 basis-point rise in the CBR can add KSh 1,500–3,000 to the monthly repayment on a KSh 3 million mortgage — money directly out of your family budget."

If you have an existing variable-rate loan, the next time you see news about the MPC meeting — held every two months — pay close attention. Those decisions are not abstract economic policy. They are your next instalment notice.

Inflation Control & the Cost of Unga

Kenyans do not need an economics degree to feel inflation. The price of a 2 kg packet of unga (maize flour), a litre of cooking oil, or a bunch of sukuma wiki tells the story better than any government bulletin. The CBK's mandate to keep inflation within a 2.5%–7.5% target band is essentially a mandate to protect the purchasing power of your Kenya Shilling.

Tools the CBK Uses to Fight Inflation

The CBK deploys several interconnected tools to manage inflation:

| Tool | How It Works | Your Day-to-Day Impact |

|---|---|---|

| Central Bank Rate (CBR) | Sets the overnight lending floor for commercial banks | Directly affects loan rates, savings rates, and mortgage costs |

| Cash Reserve Ratio (CRR) | Mandates banks to hold a % of deposits with the CBK | Limits how much credit banks can extend; controls money supply |

| Open Market Operations (OMO) | CBK buys/sells T-bills to inject or mop up liquidity | Affects returns on savings accounts and money market funds |

| Discount Window | Emergency liquidity facility for banks in distress | Prevents bank runs that could freeze your deposits |

| Moral Suasion | CBK persuades banks to act in line with policy goals | Can moderate credit expansion without formal rule changes |

Demand-Pull vs. Cost-Push Inflation

The CBK's tools work best against demand-pull inflation — the kind caused by too much money chasing too few goods. But Kenya frequently suffers from cost-push inflation driven by drought (reducing food supply), high global fuel prices (raising transport costs), and a weak shilling (making imports expensive). The CBK is less effective against these supply-side shocks, which is why inflation can remain stubbornly high even when the CBR is elevated. This limitation is important for consumers to understand: when food prices spike after a drought, blaming the CBK alone misses the full picture.

The Exchange Rate & Your Purchasing Power

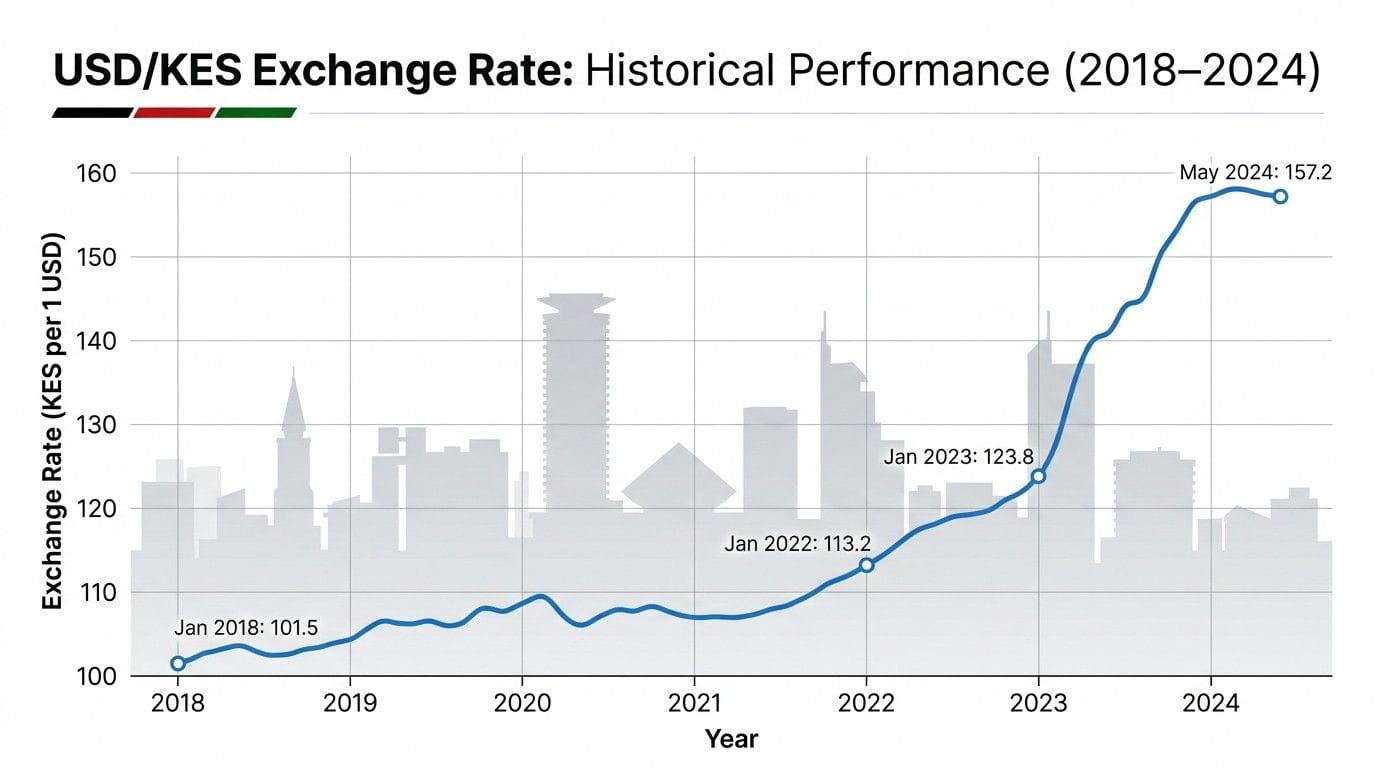

Kenya operates a managed float exchange rate regime. The CBK does not peg the shilling to a fixed value against the US dollar, but it actively intervenes in the foreign exchange (forex) market — selling dollars to support the shilling or buying dollars to replenish reserves — to smooth out excessive volatility.

Why does this matter to you, personally?

Kenya is a net importer of fuel, cooking oil, wheat, fertilisers, and machinery. When the shilling weakens against the dollar — as it did dramatically in 2023, hitting a historic low of around KSh 160 per dollar — import costs rise, and those costs cascade through supply chains directly onto supermarket shelves and petrol stations. A weaker shilling means:

- Higher petrol and diesel prices → more expensive matatu fares

- Costlier imported cooking oil and wheat → pricier chapatis and bread

- Expensive fertilisers → higher prices for locally grown produce

- Larger debt service payments on Kenya's dollar-denominated foreign loans

Conversely, a stronger shilling benefits importers and consumers but can hurt exporters like tea, coffee, and flower growers — a classic central banking tightrope act. The CBK's management of forex reserves (ideally above four months of import cover) is therefore not just an accounting exercise. It is a shield protecting the cost of your daily life.

Regulating M-Pesa & Kenya's Digital Finance Revolution

Kenya is globally celebrated for pioneering mobile money. Over 35 million Kenyans use M-Pesa, and billions of Kenya Shillings flow through the platform daily. But who ensures that your KSh 5,000 float is safe? The CBK.

Under the National Payment System Act and the Payment Service Providers Regulations, the CBK licenses and supervises all payment service providers — including Safaricom (M-Pesa), Airtel Money, T-Kash, and bank-linked wallets. Its regulatory powers include:

The Float Rule: Protecting Your Digital Cash

One of the CBK's most important (and least discussed) rules is the e-float requirement: mobile money operators must hold an equivalent amount of real money in a trust account at a CBK-supervised bank for every Kenya Shilling of digital float in circulation. This means the KSh 2,000 sitting in your M-Pesa is backed by actual cash held in trust. Without this rule, mobile money operators could theoretically issue more digital money than they hold — creating a fragile, Ponzi-like system. The CBK prevents this.

The Push Towards a Digital Kenya Shilling

The CBK has been studying the feasibility of a Central Bank Digital Currency (CBDC) — essentially a digital version of the Kenya Shilling issued directly by the central bank. A CBDC would potentially reduce transaction costs, increase financial inclusion in rural areas, and give the CBK more direct control over monetary transmission. While no launch date has been announced, this is a development worth tracking for every Kenyan who uses digital money — which, in 2026, is nearly everyone.

Keeping Your Bank Safe: Supervision & Deposit Protection

Remember the collapse of Chase Bank Kenya in 2016, or Imperial Bank in 2015? Those painful episodes — which left thousands of depositors scrambling — happened despite CBK oversight, but they also demonstrated what happens when supervision lapses. Since then, the CBK has significantly tightened its supervisory framework.

Today, the CBK requires all commercial banks to maintain a minimum core capital of KSh 1 billion (with proposals to raise it to KSh 10 billion to strengthen financial resilience). Banks must also maintain a Capital Adequacy Ratio and publish regular financial statements. The CBK conducts on-site and off-site surveillance of every licensed bank, looking for signs of financial stress before they become crises.

The Deposit Protection Fund (DPF)

Closely linked to the CBK is the Kenya Deposit Insurance Corporation (KDIC), which protects depositors up to KSh 500,000 per depositor per institution in the event of a bank failure. If you keep your savings in a CBK-licensed bank and that bank collapses, you are insured up to that amount. This protection is funded by premiums paid by all licensed banks — a collective insurance pool backstopped by regulatory oversight.

The practical takeaway: when choosing where to keep your savings, always verify that your bank or SACCO is regulated by the CBK (for banks) or the SACCO Societies Regulatory Authority (SASRA). A licensed institution means you have recourse. An unlicensed one — including many pyramid and online "investment" schemes — offers you nothing.

Government Borrowing, Treasury Bills & Your Tax Burden

Every time the Kenyan government needs money it does not have — to build roads, pay teachers, fund the military — it borrows. And one of the most important mechanisms for that borrowing passes directly through the CBK's infrastructure: the primary auction of Treasury bills (T-bills) and Treasury bonds (T-bonds).

The CBK acts as the government's fiscal agent, conducting weekly T-bill auctions (91-day, 182-day, and 364-day papers) and periodic bond issuances. When you invest in a money market fund or a bank fixed deposit, a large portion of your money is almost certainly sitting in these government securities. The rate of return on T-bills — which the CBK influences through its liquidity management — therefore directly affects the returns on your savings products.

The Debt-Inflation Trap

Here is where monetary and fiscal policy collide in a way that hits your wallet hard. When Kenya borrows excessively, interest payments crowd out public spending on services. If the government struggles to repay debt, pressure mounts on the CBK to "monetise" the debt — essentially printing more money — which fuels inflation and erodes the purchasing power of your Kenya Shilling. The CBK's independence is therefore crucial: a central bank that resists government pressure to print money protects citizens from hyperinflationary spirals seen in other countries.

"Government debt is not an abstract spreadsheet entry — it is a deferred tax on every Kenyan citizen. The CBK's role is to ensure that deferred tax does not become devalued savings."

CBK Central Bank Rate — History at a Glance

Tracking how the CBR has moved over the years helps you understand why your loan repayments — or your savings returns — changed at various points. Here is a summary of key CBR milestones:

| Period | CBR (%) | Context | Impact on Borrowers |

|---|---|---|---|

| 2011–2012 | Up to 18% | Severe inflation, shilling crisis | Loan rates soared; many borrowers defaulted |

| 2014–2016 | 10%–11.5% | Relative stability; interest rate cap debate | Moderate borrowing costs |

| 2016–2019 | 9%–10% | Rate cap era — commercial rates legally capped | Cheap credit for formal employees; SMEs locked out |

| 2020 (COVID) | 7% (cut) | Pandemic stimulus; economic rescue | Cheaper loans; moratoriums on existing facilities |

| 2022–2023 | 10.5%–13% | Post-COVID inflation; shilling weakening | Loan repayments rose sharply; cost of living surged |

| 2024–2025 | Gradually easing toward 11% | Inflation moderating; CBK cautious easing | Slight relief for variable-rate borrowers |

Frequently Asked Questions

What does the Central Bank of Kenya actually do?

How does the CBK base rate affect my loan repayments?

How does the CBK control inflation in Kenya?

Does the CBK regulate M-Pesa?

Is my money safe if my bank collapses in Kenya?

Will Kenya get a digital shilling (CBDC)?

The Bottom Line

The Central Bank of Kenya is not a distant institution populated by economists in suits making abstract decisions on a whiteboard. It is the invisible hand inside every financial transaction you make — the force that sets the price of your debt, the value of your savings, the stability of your digital wallet, and the purchasing power of every Kenya Shilling you earn.

Understanding how it works does not require an economics degree. It requires recognising a few simple truths:

- When the CBR rises, prepare for higher loan repayments.

- When the shilling weakens, brace for pricier imports.

- When inflation is high, your real wage falls even if your nominal salary stays the same.

- When you use M-Pesa, the CBK's regulatory guardrails protect every transaction.

- When you choose a bank, the CBK's supervision and KDIC insurance are your safety net.

Stay informed. Follow MPC meeting outcomes. Understand what CBR changes mean for your loan. Diversify your savings across regulated institutions. And if you are building a business or planning a major purchase, factor in the currency risk that comes with a freely floating — but managed — Kenya Shilling.

Financial empowerment in Kenya begins with understanding the institution that sits at the centre of it all.

Want More Kenyan Financial Guides?

Explore our in-depth guides on managing money, understanding taxes, and finding the best deals across Kenya. KE Offers breaks down complex topics into clear, actionable information.

Browse All Guides →Written by

KE Offers Editorial Team

KE Offers covers the Kenyan consumer landscape — from financial education and automotive guides to the best deals across e-commerce. Our editorial team verifies facts against primary sources including CBK publications, KNBS data, and official government sources.

Disclaimer: This article is for informational and educational purposes only. It does not constitute financial, investment, or legal advice. Interest rates, CBK policies, and regulatory limits are subject to change. Always consult a licensed financial advisor or visit the official CBK website for the most current information.